Canada’s economy was 1.1% below pre-pandemic levels in March 2021

After experiencing its steepest decline in decades, the economy is getting close to returning to its pre-pandemic level of output.

When the pandemic reached Canada in March 2020, the economy crashed. It registered a sizeable drop in real GDP in both March and April.

Since then, it has been on a steady upward trend despite significant second and third waves of new COVID-19 cases.

That upward trend is expected to have come to an end in April, with preliminary estimates showing that GDP declined that month in response to renewed public health measures, such as the prolonged stay-at-home order in Ontario.

The decline in output is expected to be short-lived, though, as public health measures eased in many parts of the country in May and June.

Further, Canada’s vaccine rollout has accelerated rapidly over the past few weeks, suggesting better days ahead.

Real GDP, January 2007 to March 2021 Billions, chained $

Source: Statistics Canada

Employment struggles to return to pre-pandemic levels

Employment fell for a second consecutive month in May 2021, with 517,100 fewer Canadians employed compared to February 2020. Despite the drop, 2.1 million more were employed this May compared to the same month last year.

The labour market recovery remains highly uneven across industries, regions, and population groups. Employment in industries most affected by the pandemic closures continues to lag as Ontario’s stay-at-home order curtailed activity in that province, Nova Scotia entered a lockdown at the end of April, and both Alberta and Manitoba introduced tighter measures in early May.

March 2021 saw an increase in the year-over-year change in employment for the first time since the start of the pandemic. Close to 2.5 million more Canadians were employed in April 2021 than in April 2020, and 2.1 million more in May 2021 compared to May last year.

The unemployment rate was little changed in May 2021, rising to 8.2% from 8.1% in April.

Most of the employment decline in May was due to decreases in part-time employment. Furthermore, 22.7% of people employed part-time in May desired full-time positions.

Total hours worked dropped by 2.7% in April and was little changed in May. Declines in industries most affected by tighter health measures were offset by improvements in educational services, and health care and social assistance. However, hours worked remained 3.8% below February 2020 levels.

Year-over-year change in employment, January 2008 to May 2021 000s of jobs

Sources: Deloitte, Statistics Canada

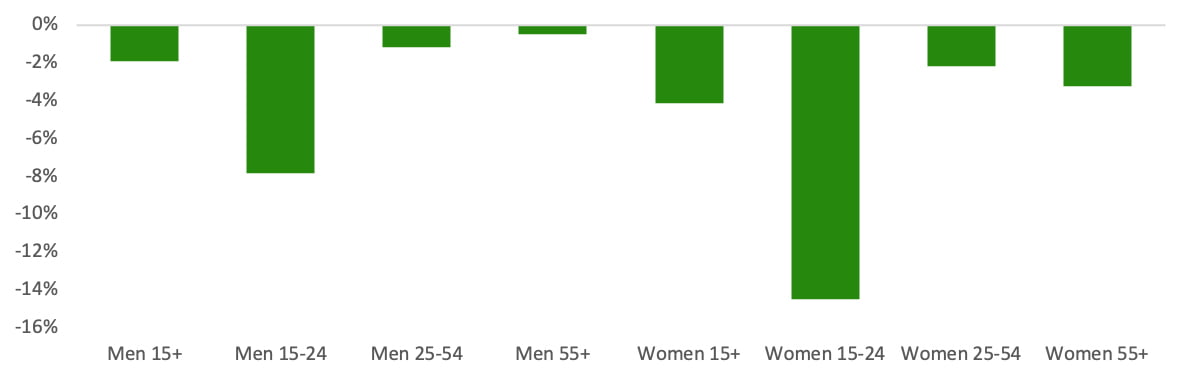

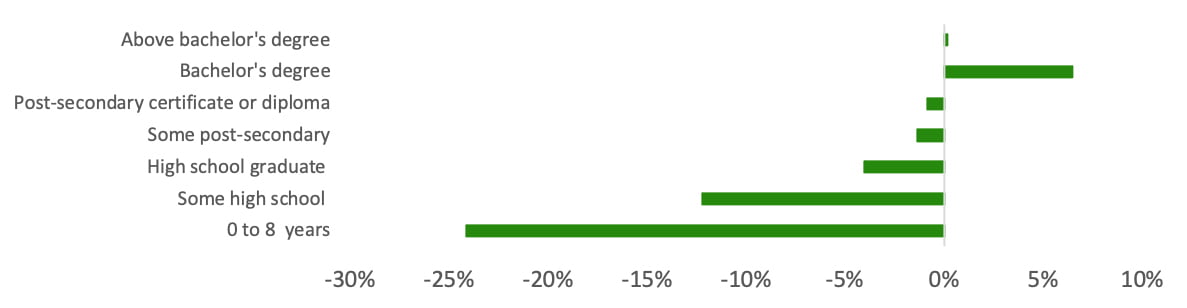

Employment changes have not been equitable across population groups

The pandemic has resulted in large increases in long-term unemployment, indicating a mismatch between supply and demand in labour.

In May 2021, nearly half a million people had been unemployed for at least 27 weeks. Many who lost their jobs in the first wave of the pandemic have since remained unemployed, leading to a surge in long-term unemployment since the fall of 2020. Chronic unemployment can lead to skills atrophy and have lasting impacts on a person’s earning ability.

Labour force participation dropped in May 2021, with youth and women aged 25 to 54 representing most of the decline. The number of individuals aged 15 to 24 participating in the labour force fell 1.3%, while the decrease among women aged 25 to 54 was by 0.6%. Unfavourable business conditions have caused many women in this age group to stop searching for work. School closures in many parts of the country are also likely to be a factor.

The employment recovery remains highly uneven across age and gender. Youth employment is the furthest from recovering, and the decline in female employment is higher than males across all age categories.

By education level, job losses are concentrated among those with lower levels. For those with a university degree (38% of the labour market), employment is 4.3% above February levels.

Employment by age and gender, February 2020 to May 2021

Employment by education, February 2020 to May 2021

Resale markets are cooling after a flurry of activity

Residential real estate has been a key driver of economic activity as we emerge from recession. After months of record-breaking movement, we’re finally seeing some cooling in the resale market.

The number of homes sold in the resale market fell in both April and May, although activity still remains at a historically high level.

New listings also fell in May, adding to the supply crunch facing the market. The number of months of inventory on the market sat at 2.1 in May, compared to a long-run average of over five.

With sales falling more than new listings, the sales-to-new-listings ratio nudged down to 75.4%. This is down substantially from the 91% in January but still over 20 percentage points higher than its long-term average. It remains firmly in sellers’ territory.

With demand remaining strong, price growth has remained firm. The average sale price was up 38.4% from May 2020 to reach $688,000, while the composite home-price index posted a 24.4% year-over-year gain.

Source: The Canadian Real Estate Association

Strong income growth continues to fuel retail spending

Retail sales bounced back quickly last year and continue to trend above pre-pandemic levels. That’s thanks to strong income growth and limits on available services.

Retail is one of the economic sectors that is heavily influenced by public health measures. At times, the sector has been negatively affected by such measures in provinces that limit in-person sales to only essential items. At other times, stores benefited from restrictions as consumers pivoted their spending away from activities like travel and dining out toward goods to enjoy at home.

This trend is evident in the sales growth by sector, with electronics, sporting goods and hobbies, building material and gardening, and cannabis stores all posting sales more than 20% above their pre-pandemic levels.

In March, we saw strong growth in retail sales as restrictions were eased between the second and third wave of the pandemic.

The preliminary estimate for retail spending in April shows a sharp drop in sales. This corresponds to health measures implemented to counteract rising case counts.

The decline should be short-lived as retailers have begun reopening across the country. However, they will face more competition for consumer dollars as other activities resume and service availability expands.

Retail sales by category % change from February 2020 to March 2021

Global recovery is boosting the demand for raw materials

We’ve seen a broad-based increase in commodity prices, benefitting many Canadian producers.

Prices for many of Canada’s key commodities have been increasing rapidly, coinciding with robust international demand as the global recovery picks up steam.

Oil prices plunged during the height of the first wave but have recovered strongly and are above their pre-pandemic levels.

We have also seen strong increases in metal and forestry prices—lumber in particular—as the housing market booms here in Canada and south of the border.

The commodity price rally pushed up Canada’s terms of trade, a key measure of our purchasing power, by 6.1% in the first quarter of the year and by 12.4% relative to the first quarter of 2020. Rising commodity prices have contributed significantly to the appreciation of the Canadian dollar.

Raw materials price index by category Index: January 2020 = 100